The demographic decline that will reshape the language school sector over the next decade will also have profound consequences for another part of the industry: ELT publishers.

For decades, the publishing market for English language coursebooks in Greece relied on a predictable structure. Each year a large number of new students entered the system, language schools adopted new Junior A series, and publishers competed for their share of that expanding or stable market.

Today, that structure is beginning to change.

The decline in births in Greece is not simply a demographic observation; it represents a structural contraction of the entry point of the ELT market. For publishers whose business model begins with the Junior A coursebook, this shift affects the entire pipeline of future students.

The size of the future Junior A market

The starting point is the number of children born each year.

In 2024, Greece recorded 68,467 births, one of the lowest numbers in modern demographic history. These children will enter primary school in 2030, and many of them will begin their first year of English in private language schools shortly afterwards.

Even if Greece maintains its strong tradition of private language education (with participation rates estimated between 60% and 80%) the total number of new Junior A students entering the system will inevitably be smaller than in previous decades.

Based on the 2024 birth sample, the potential national market for Junior A students could look roughly like this:

| Participation rate | Estimated Junior A students |

| 60% | ~41,000 |

| 70% | ~48,000 |

| 80% | ~55,000 |

These figures represent the entire national entry market for Junior A around 2030.

A striking comparison with the past

To understand the scale of the shift, it is useful to look backwards.

Twenty years ago, annual birth cohorts in Greece were often close to or above 100,000 children. The entry cohort for language schools was therefore dramatically larger. At that time, a publisher holding 30% market share could easily serve tens of thousands of Junior A students each year.

What is striking today is that the entire national market projected for 2030 may roughly equal what used to represent only a 30% share of the market two decades ago. In other words, what once represented a large publisher’s share of the market may soon resemble the size of the entire market itself.

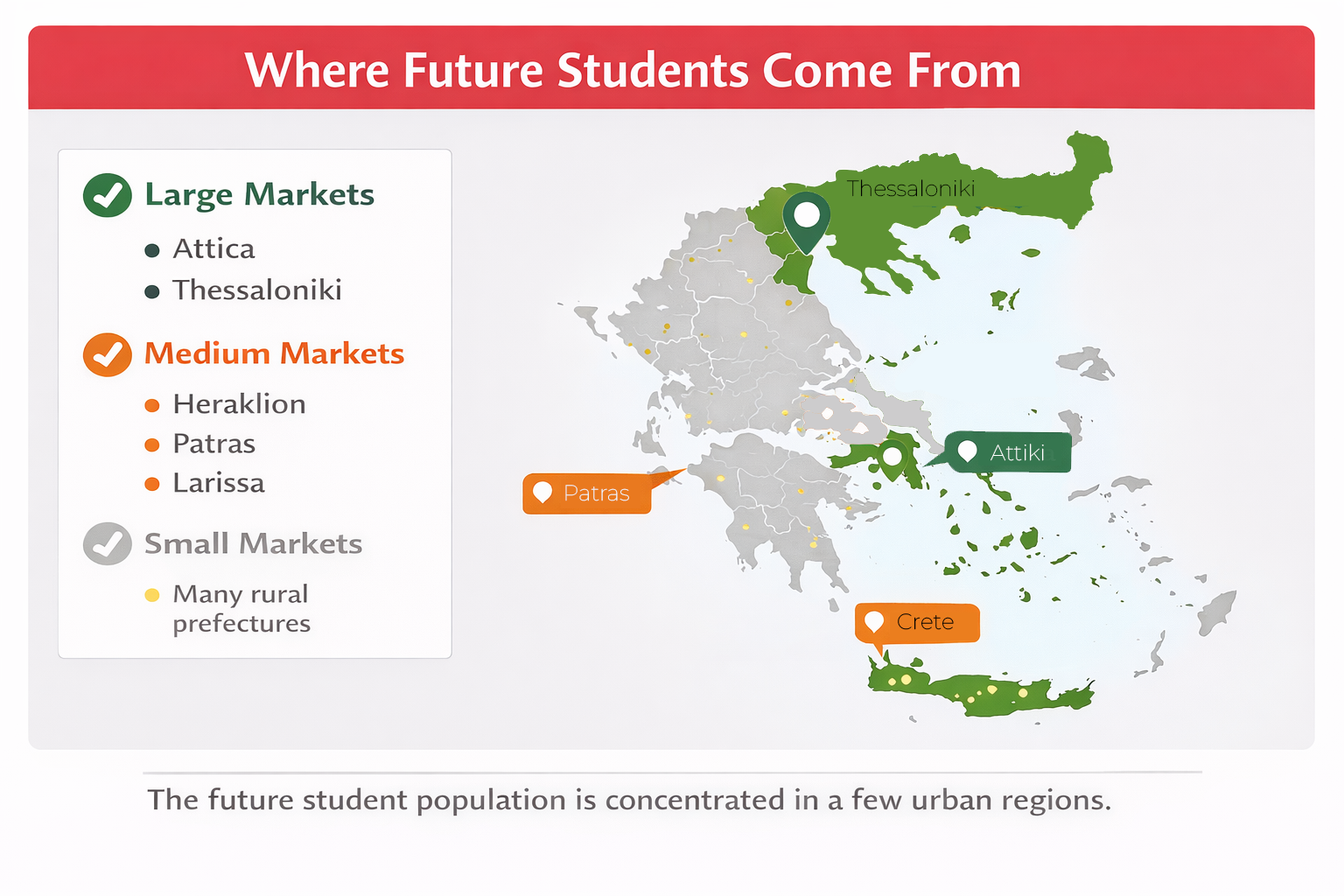

Regional markets will diverge

The demographic contraction will not affect every part of Greece equally. Births are heavily concentrated in a relatively small number of regions.

The largest future markets will remain. The lion’s share will be Athens and Thessaloniki followed byHeraklion, Patras and Larissa.

In many smaller prefectures, however, the number of births has already declined significantly. In these areas the potential pool of future students may become very limited, which will inevitably affect both language schools and the publishers supplying them.

For publishers, this means the traditional nationwide adoption strategy may gradually give way to a more regionally differentiated market.

You can’t have your cake and eat it too

In the 80s, 90s and 00s publishers grew aggressively. A healthy market size leaves room for companies to grow without displacing one another. When there is room for growth then everyone is happy. In a shrinking market, however, the dynamics change. Every new adoption gained by one publisher is almost certainly an adoption lost by another.

This intensifies competition at the Junior A level, because this is where the long-term learning pathway begins. The first coursebook adopted by a school often determines the sequence of books that will follow for several years.

Securing that first level has always been important. In a shrinking market, it becomes even more critical.

Searching for new sources of growth

The demographic contraction raises an unavoidable strategic question for publishers:

Where will future growth come from?

If the traditional language school entry market continues to shrink, publishers may increasingly need to explore new opportunities beyond the established model.

Possible avenues could include:

- international education pathways such as IB programmes

- the re-introduction of market coursebooks in the pubic sector, allowing schools greater flexibility in choosing materials

- digital learning ecosystems that expand the traditional coursebook model

- set eyes abroad

Without the development of new markets of this kind, publishers may remain confined to a sector whose size is steadily declining.

The survival of the fittest

The demographic decline is not temporary. It is not like fuel prices, fluctuating up and down. The children who will enter Junior A classes in the coming years have already been born. This means that the size of the future market is largely predetermined.

As a result, the ELT publishing sector may be entering a period in which publishers find themselves fighting for a share in a shrinking market.

Competition will intensify. Adoption decisions will become more consequential. And differentiation — whether through content, methodology, or educational ecosystems — will become increasingly important.

In many respects, the coming years may resemble a classic economic dynamic: the survival of the fittest.

Cash has always been king

In a shrinking market, financial resilience becomes more important than market presence.

When markets grow, publishers can afford aggressive marketing, wide distribution, constant promotional activity and participation in every event, because new students constantly replenish the system.

When markets shrink, the key question becomes: Which companies can maintain healthy cash flow?

The publishers who will still be present in a decade will most likely be those that maintain strong financial discipline, protect profit margins, avoid unnecessary spending and invest strategically rather than symbolically.

In other words, survival will be determined as much by financial management as by editorial quality.

The End of Symbolic Spending

A shrinking market inevitably forces companies to reassess how they allocate resources.

Activities that once felt essential for visibility may come under scrutiny, such as:

- participation in multiple regional exhibitions

- attendance at every local event

- ceremonial gatherings or social functions

- sponsorships whose commercial impact is difficult to measure.

In an environment where the number of potential students is declining, the return on these activities may no longer justify the expense.

Publishers may therefore become more selective and more strategic about where they invest their marketing budgets.

However, cost-cutting does not necessarily mean disengagement. If anything, the opposite may occur. In a shrinking market, relationships become more valuable than exposure.

Publishers who succeed will likely focus less on broad promotional visibility and more on:

- strengthening relationships with language schools

- supporting teachers and directors of studies

- providing meaningful pedagogical support

- building long-term partnerships rather than transactional sales.

In other words, the future competitive advantage may lie not in being everywhere, but in being truly valuable to the customers who matter most.

The Industry May Become Smaller, but Stronger

This process often leads to an industry that is smaller in size, but more disciplined and more focused on long-term sustainability.

Some publishers may reduce their presence, exit the market or focus in other global markets. Others will adapt and refine their strategy. The companies that remain will likely be those that combine educational quality with financial discipline and strong customer relationships.

In that sense, the phrase used earlier in the article may prove accurate. The coming decade may indeed resemble a period of survival of the fittest, not only in terms of products, but also in terms of financial resilience and strategic focus.

A personal perspective

The analysis presented in this article reflects my personal interpretation of the available data and how I perceive the market may evolve in the coming years.

Demographic trends are clear, but the way the sector responds to them is not predetermined. Markets are shaped not only by statistics but also by the decisions, creativity, and strategic thinking of the people working within them.

For that reason, this article should not be read as a final verdict, but rather as the starting point for a broader discussion within our industry.

I would very much welcome the perspectives of colleagues .

How do you see the market evolving?

What opportunities do you believe still exist?

And what strategies will help our sector remain vibrant in the years ahead?

Your ideas, insights, and experiences are an essential part of this conversation. Join in at editorial@eltnews.gr